By: Robert Kleinhenz, Deputy Chief Economist

The median price in California continued to increase in September, driven by lean inventory levels, while home sales remained on track with expectations for the month. The median price of a detached existing single family home was $296,090 in September, up 1.1 percent from the August median of $292,960, but down 7.3 percent from the September 2008 median price of $319,310. Barring a sudden decline in home values over the next few months, the statewide median price will register year-over-year gains by year end, although it will still be well below the mid-decade peak.

Sales in California hit 530,520 homes in September, up 0.6 percent from August sales of 527,120 homes, and up 2.1 percent from September 2008 sales of 519,530 homes. With sales expected to stay in the low- to mid-500,000 range through the rest of the year, annual sales for 2009 will finish about 20 percent higher than the 2008 annual sales figure of 439,830 homes.

Given recent price gains and sales levels, as well as lean inventory numbers that have averaged just over 4 months for the past 3 months, one should conclude that the California housing market is edging back toward its normal state. Indeed, these numbers are welcome developments for a housing market that was among the hardest hit in the country. But a look behind the topline numbers suggests that current conditions have resulted from a heavy dose of policy intervention and from efforts by lenders – who currently dominate the supply side of the market – to manage the flow of troubled mortgages and properties at all stages of the ‘foreclosure pipeline’ from delinquencies to REOs.

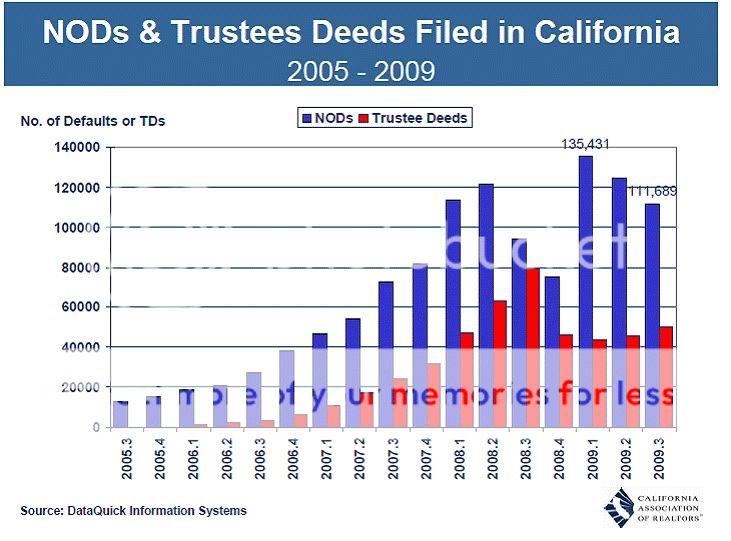

The number of defaults in California escalated rapidly in the last couple of years, with 111,700 defaults in the third quarter of this year and a record high of 135,400 defaults in the first quarter of 2009. Normally, the trend in foreclosures corresponds approximately to the trend in defaults with a one to two quarter lag so the number of foreclosures should be on the rise as well. Instead, the level of foreclosures has been steady at roughly 50,000 per quarter since the last quarter of 2008. This seems to be the result from the combination of policy intervention, including foreclosure moratoria last year and early this year as well as the federal loan modification program, and efforts by lenders to deal problem loans on a case-by-case basis. As a result, market supply has held steady at levels that have stabilized the median price at the state level and in most California markets. In a number of markets, there have been some modest price gains compared to earlier in the year.

With current government policies and lender practices in place, home prices in much of the state should hold steady, aside from normal seasonal fluctuations in prices between now and next spring. In the end, price stability is necessary for discretionary sellers, as opposed to distressed sellers, to return to the market and drive the supply side of the market to more normal conditions.